The Complete Trump Account Guide

How to open one, claim every available contribution, let family give through a link or QR code, and decide where your own dollars belong.

Open the account for every eligible child. Claim every legitimate government, employer, or donor dollar available. Use it confidently for gifts meant to stay invested. Then choose the next account based on what the money is actually for.

Trump Accounts are live, and the opportunity is broader than the headline suggests. Some young children can receive $1,000 from Treasury. Older children may still qualify for employer or philanthropic contributions. And the official app gives parents a surprisingly clean way to turn birthday checks and "what can we get the baby?" texts into long-term investments.

This is not a replacement for every account a family already uses. A 529 can still be better for college. A Roth IRA can be exceptional once a teenager has earned income. The case for opening a Trump Account is simpler: it costs nothing to open, it can receive money your child cannot get anywhere else, and opening it preserves options.

What this guide covers

Six decisions, in the order a family will actually encounter them.

File Form 4547 in the official app or through the IRS. Activate the account when Treasury confirms it. Claim the $1,000 if your child meets the narrower pilot rules. Ask HR and check the app for donor money. Use the child-specific invite link for long-term gifts. Keep family contributions under the shared $5,000 annual cap and save the annual tax form.

Open it before you optimize it

The setup has two parts: make the election, then activate the investment account.

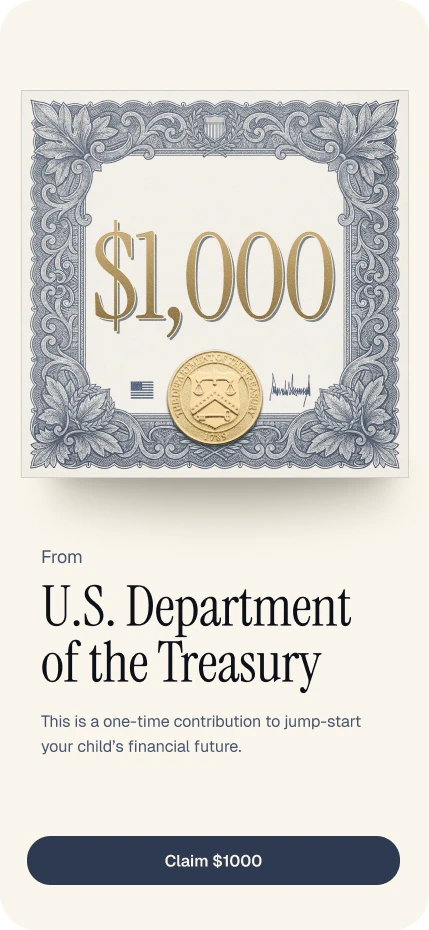

A child under 18 with a valid Social Security number can generally have a Trump Account opened for them. The federal $1,000 has a narrower gate: the child must be a U.S. citizen with an SSN and must have been born from January 1, 2025 through December 31, 2028.[1]

File the election

Use the Trump Accounts app, the web app, or the IRS. The app can complete and submit IRS Form 4547 after identity verification.

Have your legal name, SSN or ITIN, address, phone, email, government ID, and the child's legal name, SSN, date of birth, relationship, and address ready.

Choose the $1,000 election if eligible

The account election and the pilot contribution election are separate boxes. An older child can still have an account even when they do not qualify for Treasury's $1,000.

Wait for the activation notice

After the IRS processes the election, Treasury sends an email and in-app notification. The official activation email comes from no-reply@trumpaccounts.treasury.gov.

If Form 4547 went in with your 2025 return, you do not need to submit it again while the election is processing.

Fund it, or leave it alone

Once activated, link a bank account or supported debit card. You can make one-time or recurring contributions, view balances and history, and manage multiple children from one login.[2]

Before a co-parent or grandparent starts a second application, confirm that nobody has already filed for the child. A prior Trump Account election blocks another initial election.

What happens to the money

At launch, contributions are automatically invested in SPYM, a low-cost S&P 500 ETF. Treasury also selected IVV, VTI, SPTM, and ITOT for future investment choices. All are broad U.S. stock index funds. There is no clever fund-picking exercise hiding here.[3]

Until the end of the year before the child turns 18, withdrawals are generally blocked. The narrow exceptions cover trustee-to-trustee rollovers, certain ABLE rollovers at age 17, excess contributions, and death. Put money here only if you can leave it alone.

The free money is the reason to open it

A child can miss the federal $1,000 and still have a compelling reason to own the account.

The headline number belongs to newborns. The account itself is available much more broadly, and an open account is the admission ticket for employer, government, charity, and donor programs.

The federal pilot deposit

For an eligible U.S. citizen child with an SSN born in 2025, 2026, 2027, or 2028. It does not count against the normal $5,000 annual cap.

LiveA new family benefit

An employer can contribute under a written Trump Account program. Up to $2,500 per employee, across the employee's children, can be excluded from the employee's income. It still counts toward each child's shared $5,000 cap.

Committed by 50+ companies; support center says funding is coming soonA large ZIP-code program

Michael and Susan Dell committed $6.25 billion for the first 25 million children age 10 and under living in ZIP codes with median incomes below $150,000. The gift is aimed at children who do not receive Treasury's $1,000. Check the app for eligibility and timing.[4]

AnnouncedCharities and governments

Qualified nonprofits and governments can fund a defined group, such as children in a state, county, ZIP code, birth year, or other permitted class. Those qualified general contributions sit outside the normal $5,000 cap.

Program-specificStart with HR: "Does our company have a Trump Account contribution program?" Then check the app for charitable or government deposits. Outside money is the scarce part. Your own savings can always go into a 529, Roth IRA, or custodial account later.

Why the donor channel could get much larger

Treasury now accepts large gifts of readily tradable public-company stock for eligible Trump Account programs. That creates a practical route for founders and executives whose wealth is concentrated in company shares, not cash. Qualified charities and governments must contribute to an eligible class rather than choose a single familiar child.[5]

The QR code turns a good intention into a deposit

The most useful contribution link is not on this page. It is the one created for your child inside the official app.

Open the child's account, choose the option to invite loved ones to contribute, and share the official link or QR code the app generates. A grandparent or friend can then contribute without asking for an account number or mailing a check.

The exact labels may change as the app evolves. The rule does not: use only the child-specific path created inside the official Trump Accounts app. Never send a child's SSN, birth certificate, login code, or account screenshot to a giver.

The QR that matters is personal

The codes below can open the official site, the election path, or this guide. They cannot fund your child. Only the official app can create that child's contribution invitation.

That is the link to place in a birth announcement, save for birthday replies, or send when someone asks what the child needs.

Is this a great birthday gift?

Yes, when the gift is supposed to grow. Not automatically, when the money already has a near-term job.

- The giver wants the money invested for years.

- The child does not need access before 18.

- The family is under the shared $5,000 annual cap.

- The gift would otherwise become unassigned cash.

- The child is meant to spend it now.

- The money is clearly for education and a 529 offers better tax treatment.

- The child has earned income and a Roth IRA is available.

- Flexibility before 18 matters more than tax deferral.

What happens tax-wise when Grandma sends $100

The $100 is not income to the child. It is a nondeductible gift from the giver and generally creates basis in the Trump Account. The money can then grow without annual tax bills while it stays invested. After the account becomes a traditional IRA, the earnings and any dollars without basis are generally taxable when withdrawn.

For normal birthday amounts, federal gift tax is rarely the constraint. The IRS now provides a reporting safe harbor for qualifying Trump Account gifts when its conditions are met, including that the donor's total gifts to the child stay within the 2026 annual exclusion of $19,000. The Trump Account itself can accept only $5,000 in combined private and employer contributions for the child that year, so the account cap usually arrives first. A giver making other or larger gifts to the same child should check the safe-harbor details.[6]

My practical answer for family and friends: this is one of the better places to send a modest gift that is explicitly meant to become the child's future money. Say that out loud. "We are investing birthday gifts for her. Here is the official link."

Official starting pointApp download, eligibility, and current program information.

Open TrumpAccounts.gov Election path

Election path Share this guide

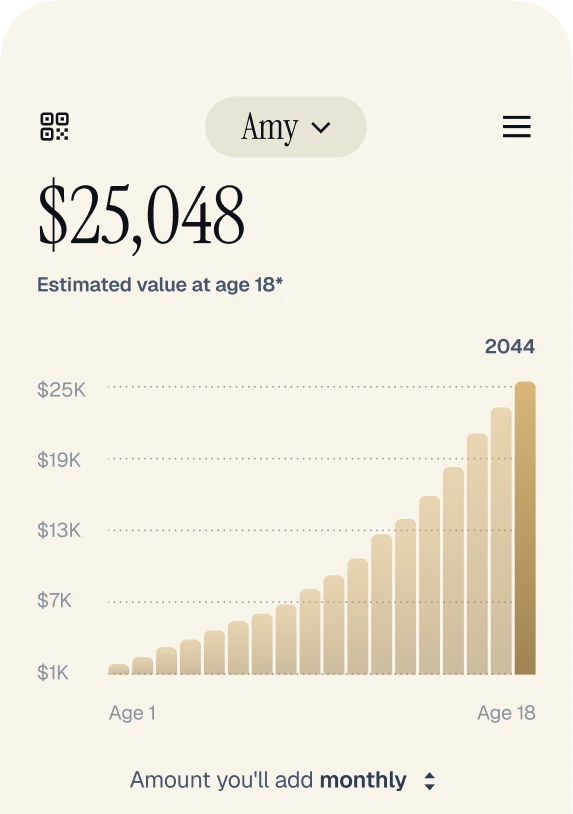

Share this guideSmall money gets interesting when it gets time

Start with the $1,000 pilot deposit. Then add a yearly birthday gift and watch the balance separate from the dollars contributed.

Family compounding calculator

Change any input. The chart updates instantly.

Four buckets of money, two tax treatments

The only recordkeeping question that really matters is whether a contribution creates basis.

No contribution is taxable income to the child when it goes in. The difference shows up later. Family money has already been taxed and generally creates basis. Federal, qualified charity or government, and qualifying employer money does not create basis.

| Money source | Counts toward $5,000 cap? | Creates basis? | What to remember |

|---|---|---|---|

| Federal $1,000 | No | No | Taxable under IRA rules when eventually distributed. |

| Qualified charity / government | No | No | Must be made through a qualified class program. |

| Employer | Yes | No | Up to $2,500 per employee can be excluded from employee income. |

| Parent, friend, child, grandparent | Yes | Yes | Nondeductible, after-tax contribution. Keep the annual record. |

Save each Form 5498-TA and account statement. The trustee is required to report contributions and basis, but your family's copy is the backup that can prevent a future distribution from being taxed incorrectly.

What changes at 18?

Starting January 1 of the year the child turns 18, most of the special growth-period rules end and the account generally follows traditional IRA rules. Taxable withdrawals are ordinary income. A 10% additional tax can apply before age 59 1/2 unless an exception applies, including certain higher-education costs or up to $10,000 for a qualifying first-home purchase.

Can the account be converted to a Roth IRA?

Once ordinary traditional IRA rules apply, a conversion to a Roth IRA may be available. The taxable portion converted is generally income in the conversion year. A low-income year in early adulthood can make a partial conversion worth examining, but basis across traditional IRAs and the child's broader tax picture matter. This is a planning conversation, not an automatic move.[7]

Is the gift deductible for the giver?

No. A personal contribution from a parent, relative, friend, or the child is not an income-tax deduction. It generally creates basis in the child's account instead.

What about state taxes?

Federal rules do not guarantee identical state treatment. Check your state's rules, especially before a conversion or withdrawal. A 529 may also carry a state deduction or credit that changes the next-dollar decision.

Opening the account is easy. Funding it is a choice.

Once the free and outside money is captured, match your own dollar to its job.

A Trump Account is strongest as an open door: Treasury money, an employer benefit, a community program, and family gifts intended to compound. It is not automatically the best destination for every dollar a parent saves.

| Account | Best use | Main tradeoff | Rule of thumb |

|---|---|---|---|

| Trump Account | Outside contributions and long-term family gifts | Locked during childhood; traditional IRA tax rules later | Open it. Capture available money. Be selective with your own. |

| 529 plan | Education from school through college and credentials | Nonqualified withdrawals can create tax and penalty on earnings | Usually the first stop for money clearly meant for education. |

| Custodial Roth IRA | A child with documented earned income | Contribution cannot exceed eligible compensation or the IRA limit | Hard to beat once a teenager has real pay. |

| UGMA / UTMA | Flexible investing with no required purpose | Irrevocable gift; child gains control at the state's age | Use when flexibility matters more than control and tax shelter. |

529 plan: still the education workhorse

Contributions are after-tax, but qualified education withdrawals are federally tax-free and many states offer deductions or credits. The owner keeps control and can often change the beneficiary. Long-held accounts may also roll limited amounts to the beneficiary's Roth IRA, subject to the 15-year, annual-limit, five-year-lookback, and $35,000 lifetime rules.[8]

Custodial Roth IRA: exceptional once a child works

A parent can open a custodial Roth IRA, but the contribution requires the child's taxable compensation. Babysitting, lawn work, modeling, or a family business can qualify only when the work and pay are legitimate and documented. Contributions come out first under Roth ordering rules; qualified earnings can be tax-free later.

UGMA / UTMA: flexible, but the gift is permanent

The custodian can invest for the child and spend for the child's benefit. The assets legally belong to the child, who gains control at the applicable age. Investment income can face kiddie-tax rules, and the account may weigh more heavily in financial-aid formulas than a parent-owned 529.

Coverdell ESA: useful, but narrow

A Coverdell can pay qualified elementary, secondary, and higher-education expenses. The annual contribution limit is $2,000 per beneficiary, contributor income limits apply, and remaining funds generally need action by age 30. A 529 is simpler for most families, but a Coverdell can offer broader investment choice.

ABLE account: a specialized and powerful option

For an eligible person with a disability, an ABLE account can support qualified expenses while protecting access to certain public benefits. It belongs in the supplemental toolkit, not the core recommendation for every family.

Trusts and savings bonds: situational tools

Trusts can preserve control and define terms for larger gifts, but they add legal, tax, and administrative cost. Series I and EE savings bonds can be simple gifts and may receive favorable education treatment when ownership, use, and income rules are met. Neither is a default substitute for the accounts above.

Who is actually putting money behind this

The program becomes more interesting as employers and donors compete to fund accounts families have already opened.

The "adopt a ZIP code" opportunity

This is not one national program. It is a repeatable pattern for a company, foundation, alumni group, hospital system, or civic organization that wants a visible local impact.

Employers already named by Treasury

Charles Schwab, Uber, Charter Communications, BNY, State Street, Mastercard, Visa, Block, Robinhood, SoFi, Chime, Russell Investments, Dell Technologies, Steak 'n Shake, Broadcom, Intel, IBM, JPMorgan, Chipotle, Coinbase, and Comcast were among the early companies Treasury identified as offering or planning matching contributions. Program designs and launch dates differ, so employees should confirm with HR.[9]

The questions families ask next

Short answers, with a primary source one click away when the details matter.

My child was born before 2025. Should I still open one?

Usually yes. They will not receive the federal $1,000 pilot deposit, but an under-18 child with a valid SSN can generally have an account and may qualify for employer, charity, government, or donor money.

Can grandparents open the account?

For opening the account without the pilot election, IRS instructions use an order of priority: legal guardian, parent, adult sibling, then grandparent. The $1,000 election has its own qualifying-child rule. In most families, a parent or legal guardian should handle the election and send grandparents the official contribution link.

Can grandparents and friends contribute directly?

Yes. Parents, relatives, friends, and the child can contribute cash. Use the official child-specific invitation generated in the app. Their combined contributions, plus employer contributions, generally cannot exceed $5,000 for the child in 2026.

Does this replace a 529?

No. A 529 is usually better for money clearly intended for education because qualified withdrawals can be tax-free. A Trump Account is attractive for outside contributions and gifts that can stay invested into adulthood.

Can the money be used for college or a first home?

Not during the growth period. After the special rules end, the account generally follows traditional IRA rules. Certain higher-education and first-home withdrawals can avoid the 10% additional tax, but the taxable portion is still ordinary income.

What if the family reaches the $5,000 cap?

The official support center says excess contributions will be declined and recurring contributions pause until the next calendar year. Qualified federal, government, charity, and rollover contributions are outside that limit. For additional family savings, compare a 529, Roth IRA if earned income exists, or a custodial account.

What fees and investments are allowed?

During the growth period, investments must be eligible broad U.S. stock index funds without leverage and with annual fees and expenses no higher than 0.1%. SPYM is the launch default; Treasury selected IVV, VTI, SPTM, and ITOT for future choice.

How do I avoid scams?

Start at TrumpAccounts.gov, the official app, or trumpaccount.com. Do not search for a support phone number in an ad. Official support is 866-USA-4547. The support team says it will never ask for your password, remote-screen software, or a payment through Cash App, Venmo, or another app.[10]

Primary sources and practical help

Start with the official app and support center. Use the tax documents only when you need the machinery underneath.