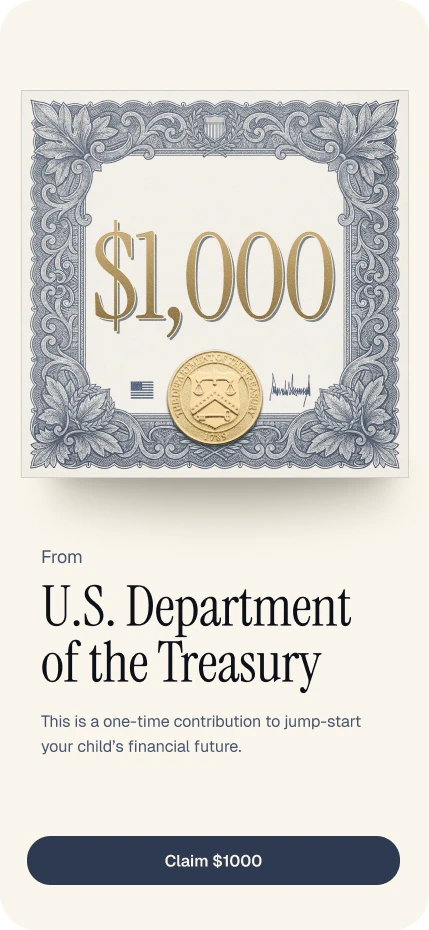

Open the account if your child qualifies. Claim whatever starter money is available.

Use it gladly for first dollars, birthday money, holiday money, and outside contributions. If relatives want to give something that can grow, this is often one of the best places to send them.

Keep the caveat simple. Employer and other private contributions generally share a $5,000 annual cap during the growth period. Gifts are not income to the child when contributed and generally create basis, but growth is still IRA-style later. Use a 529 for school money and a Roth IRA once a child has earned income.

Start with a baby, not a tax form. A child is born. Someone opens an account. A small amount of money gets invested before the child can walk, talk, or ask why the market is down. That is the trick.

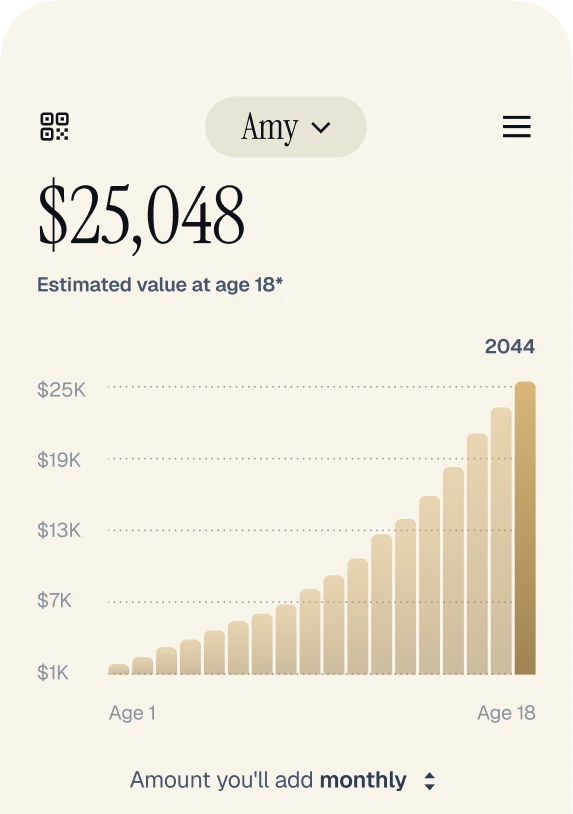

The first dollars do not have to be huge. They just have to be early. Money invested at birth has years to breathe. It has time to grow, time to fall, time to recover, and time to teach a family a better habit: own simple things early and leave them alone.

So what is a Trump Account? At its simplest, it is an investing account for a child, with special rules while the child is young. Some eligible children can receive a federal $1,000 starter contribution. Parents, relatives, employers, charities, governments, and other donors may also be able to add money, within the rules.

This is where the account really earns its place. Think about the checks that show up for birthdays, holidays, baptisms, graduations, and "we just want to help" moments. Most of that money gets spent, or it lands in a savings account and slowly disappears from everyone's attention. If the giver's intent is long-term investing, a Trump Account can be one of the best places to send it.

The tax mechanics are part of why. Contributions made during the growth period are not income to the child when they go in. Money contributed by parents, relatives, friends, and other private givers generally creates basis in the account, which matters later. The tradeoff is that after the growth period, traditional IRA rules generally apply, so investment growth can be taxable when it comes out unless an exception applies. That is a reasonable trade for decades of compounding, but it is a reason to keep records and use the account for money meant to stay invested.

The guardrails are mostly helpful. During the growth period, the investment choices are meant to be broad, low-cost, and U.S.-focused. That is not flashy. It is the point. Most families do not need fancy. They need early, simple, low-cost, and consistent.

Default rule of thumb. Open it if eligible. Claim what is available. Welcome outside contributions, and tell the people who love your child that this is where birthday and holiday money can do real work. Keep good records, especially of basis. Then pause before routing every family dollar here and ask one question: what is this money actually for? If it is for college, a 529 plan may be cleaner. If it comes from a teenager's own earnings, a Roth IRA may be better.

What Trump Accounts are. IRS Notice 2025-68 says a Trump Account is a type of traditional IRA established for an eligible individual, with special rules before the calendar year the child turns 18. Eligible children can have an initial account opened through IRS Form 4547 or the official app / online tool. For the federal pilot contribution, the child must be a U.S. citizen, have an SSN, be born after Dec. 31, 2024 and before Jan. 1, 2029, and have no prior pilot election.

Who can put money in. During the growth period, contributions may include the federal $1,000 pilot contribution, qualified general contributions from governments or 501(c)(3)s for qualified classes of beneficiaries, qualifying employer contributions, rollovers, and other family/private contributions. The normal aggregate annual limit for employer plus other private contributions is $5,000 during the growth period, with cost-of-living adjustments after 2027. Contributions cannot be made before July 4, 2026.

How it gets invested. During the growth period, investments must be eligible funds: generally mutual funds or ETFs following an index of primarily U.S. companies, without leverage, with annual fees and expenses capped at 0.1% of the balance, plus other Treasury criteria. Treasury announced SPYM as the launch default, with IVV, VTI, SPTM, and ITOT selected for the lineup once future choices are available.

When money can come out. Before the growth period ends, distributions are generally blocked except for specific cases such as rollovers, ABLE rollovers, excess contributions, and death. Starting Jan. 1 of the year the beneficiary turns 18, the account generally follows traditional IRA rules, including ordinary income taxation and the 10% early-distribution penalty unless an exception applies.

Bottom line. This is a very good place for starter, employer, charity, government, donor, and normal occasion-gift contributions meant to compound for years. It is not automatically the best place for parents' own after-tax dollars. Treat it as one useful piece, not the whole plan.

Check eligibilityConfirm SSN, citizenship status, birthdate, and whether a prior pilot election already exists.

Open the accountUse TrumpAccounts.gov, the official app, or the IRS election path once available for the child.

Save the receiptsTrack which dollars came from family after-tax money versus federal, employer, government, charity, or donor sources.

Revisit each yearBefore adding more money, check school needs, earned income, fees, and any donor or employer programs.

Start here

Start here

IRS election path

IRS election path

Share this guide

Share this guide